Short Puts Aren't For Everyone. But I'm Not Just Anyone...

By Sean McLaughlin

October 20, 2025

When markets change, we have to be quick to adapt.

I'll be the first to admit I don't always adapt as quickly as I'd like. Of course, I only know this with the benefit of hindsight. It's incredibly hard to know in the moment when it's time to pivot.

But as markets got a bit wobbly over the past week or so, I pivoted into an options strategy I haven't found opportune times to employ lately—the simple naked short put play.

Naked short puts aren't for everyone. They entail open-ended risk. You can call it unlimited risk, though technically a stock can't go below zero, so there is a limit.

And if that wasn't hard enough, the buying power requirement to hold naked short puts can be onerous—particularly for smaller accounts or if you've committed capital elsewhere.

To make it worse, your gains are capped. The most you can make is the premium you collect upfront, while you're on the hook to potentially lose multiples more if you're wrong.

Sounds like a bad deal, right?

Well, sure. In the hands of a novice (which you are not), they can be terrible deals.

But if you've been reading me for any length of time, you know we don't enter trades without a plan and without proper position sizing.

Short put trades can be excellent when done at the right time. We need two very important ingredients to make them most advantageous:

First, high implied volatility—in other words, high options premiums to collect.

Second, a significant level of nearby support that the stock should be expected to hold.

When we have both, we've got an excellent candidate. But I apply two additional filters: I only like doing these trades on sector ETFs or large-cap stocks unlikely to gap suddenly against me. And we don't want binary risk like an upcoming earnings release. That introduces risk we can't manage.

At the end of the day, it's best if you're selling puts in a stock you wouldn't mind owning at lower prices.

Check all these boxes? Game on.

Risk management is critical here. If my short puts go in-the-money—meaning the stock trades below the strike price—I'm at risk of being assigned stock at any time. This means I'd become the owner of 100 shares for every contract I sold, paying the strike price for those shares.

To keep me out of trouble, I size my put position so that in the unlikely event I get assigned stock, the total cash outlay is no more than 10% of my portfolio value.

This way, even in the very unlikely event the stock goes to zero, the worst impact to my total portfolio would be a 10% loss. That would suck, but I can come back from that. And so can you.

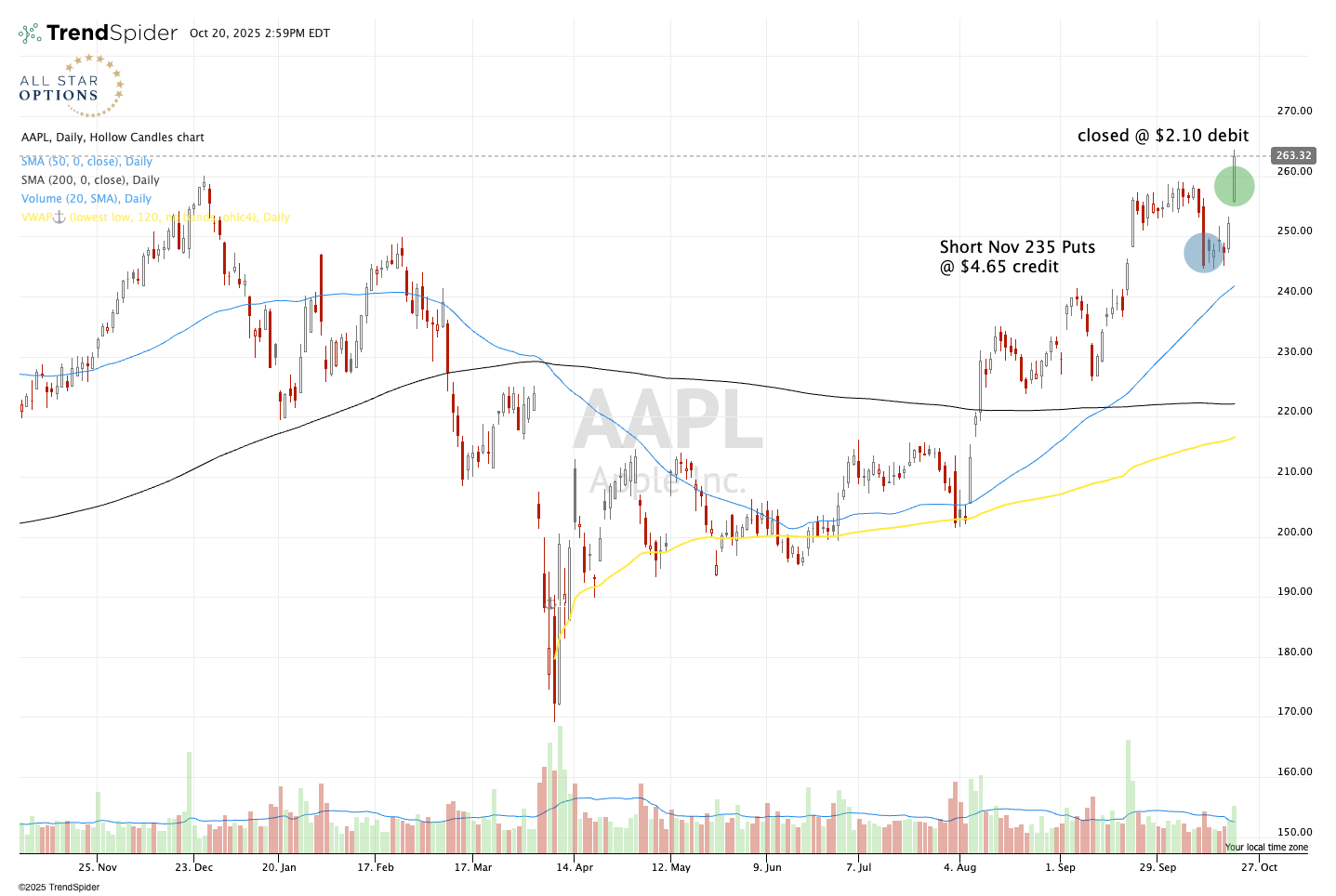

In All Star Options, we recently did exactly this trade in Apple $AAPL. On October 10th, with the stock falling and volatility rising, I noticed the rising 50-day moving average coming up to offer nearby support. Additionally, $240 had been resistance a couple months back and looked ready to flip into support.

With attractive premiums at the 235 put strike in November options, I took my shot and sold them for $4.65 per contract. I immediately put out a good-til-canceled order to buy these puts back at a profit for $2.30.

Today at the open, $AAPL gapped higher and my GTC order was filled with a bit of price improvement—getting me out at $2.10. Nice.

It only took seven trading days. I got both the direction and the volatility pullback working in my favor to pull the premium out of these puts.

Yes, naked short puts carry more risk than a typical trade I put on. But they come with significantly higher chances of success versus most trades. That's what makes the risk worth it. I'm highly likely to succeed.

There's a time and a season for every options strategy. As implied volatility rises this earnings season, I'll likely be hunting for more of these trades—after earnings reports have passed, of course.

Sean McLaughlin | Chief Options Strategist, All Star Charts