Over the past two years, the story in commodities has been pretty straightforward.

Precious metals have been the clear leaders.

Ever since Gold broke out on March 4, 2024, the entire complex has been dominated by strength in Gold, Silver, and the mining stocks.

It has been one of the cleanest and most persistent trends we’ve seen across any asset class, with capital consistently flowing into the metals while much of the rest of the commodity space lagged behind.

But markets don’t stay static forever.

Instead, they evolve and rotate.

And when leadership begins to shift, it almost always shows up first in intermarket relationships rather than in headlines.

That’s exactly what we’re seeing right now.

There are two key ratios that illustrate just how quickly the environment is changing, and both send a very similar message.

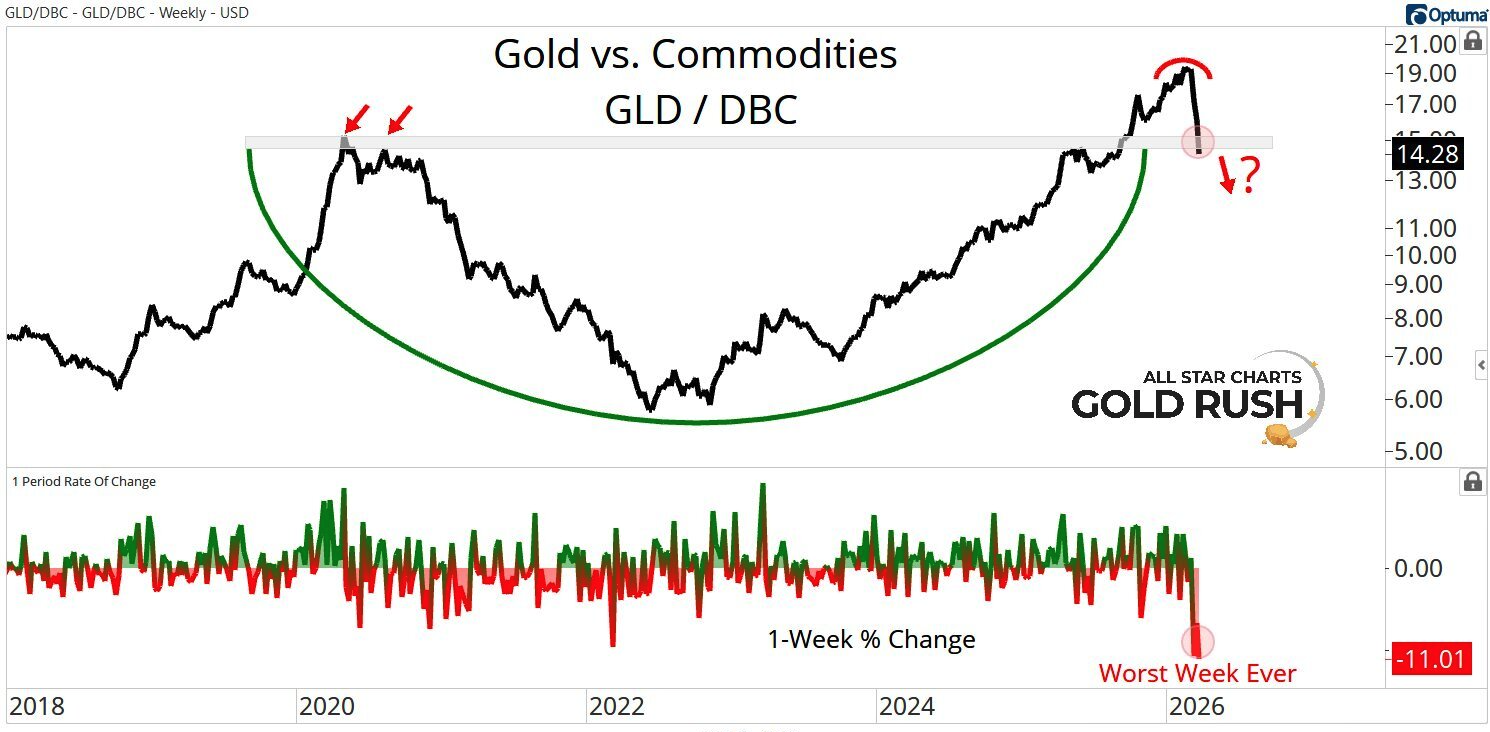

The first is Gold relative to the broader commodities complex, which we track using the ratio of the Gold ETF $GLD to the Commodities ETF $DBC.

Since bottoming in June of 2022, this ratio has been in a strong primary uptrend, with Gold outperforming the broader commodity basket by more than 200% over that period.

That kind of sustained relative strength doesn’t happen by accident. It reflects a steady demand from the world's largest financial institutions.

But last week, something changed...

This ratio broke below its prior-cycle highs, dating back to the middle of 2020.

And it didn’t just drift lower...

The ratio suffered its worst weekly decline ever, based on data going back to 2006.

That kind of move is not normal, and it’s certainly not something we see in healthy, ongoing uptrends.

Instead, it tends to occur at moments where the market is undergoing a transition, particularly when a leadership group begins to lose its relative edge.

Importantly, this doesn’t mean precious metals need to crash from here.

It doesn’t mean Gold and Silver can’t move higher in absolute terms.

What it does suggest, however, is that the period of dominant outperformance from precious metals relative to the broader commodity complex is likely behind us, at least for now.

Supercycle Report highlights the breakout setups, rotations, and technical signals shaping metals markets — giving traders an edge in gold, silver, and commodities.