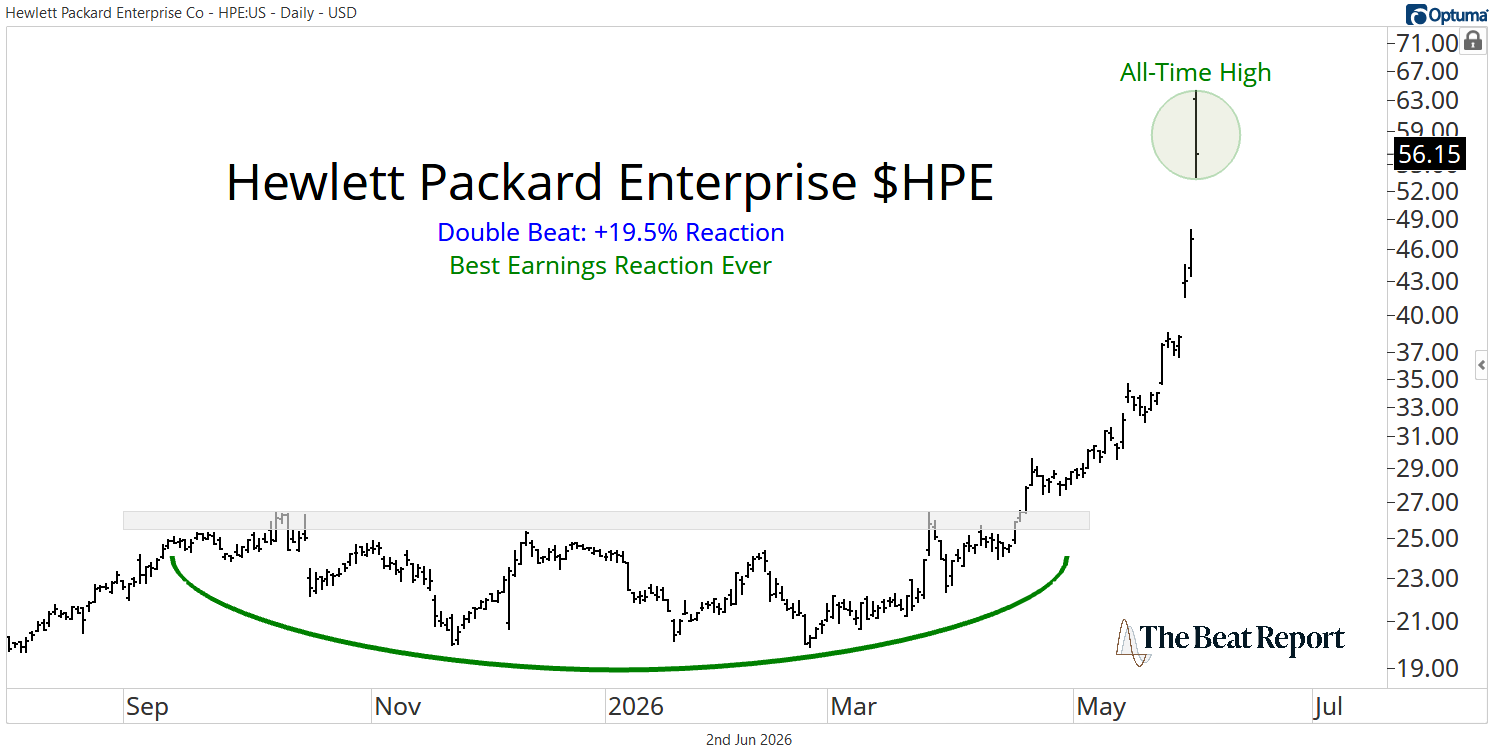

It just had its best earnings reaction ever and closed at a new all-time high.

June 3, 2026

Enterprise hardware stocks rarely trade like this...

Hewlett-Packard Enterprise $HPE is not a meme stock or a tiny biotech. This is a mature enterprise technology company that was once easy to ignore.

But not anymore...

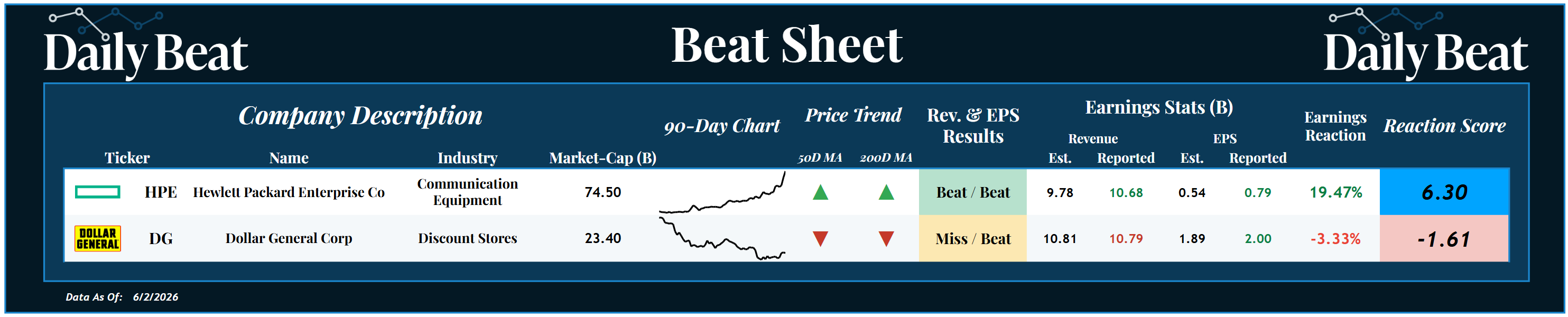

On Tuesday, HPE ripped nearly 20% after crushing Wall Street’s expectations, marking the best earnings reaction in the stock’s history, and the price closed at a fresh record high.

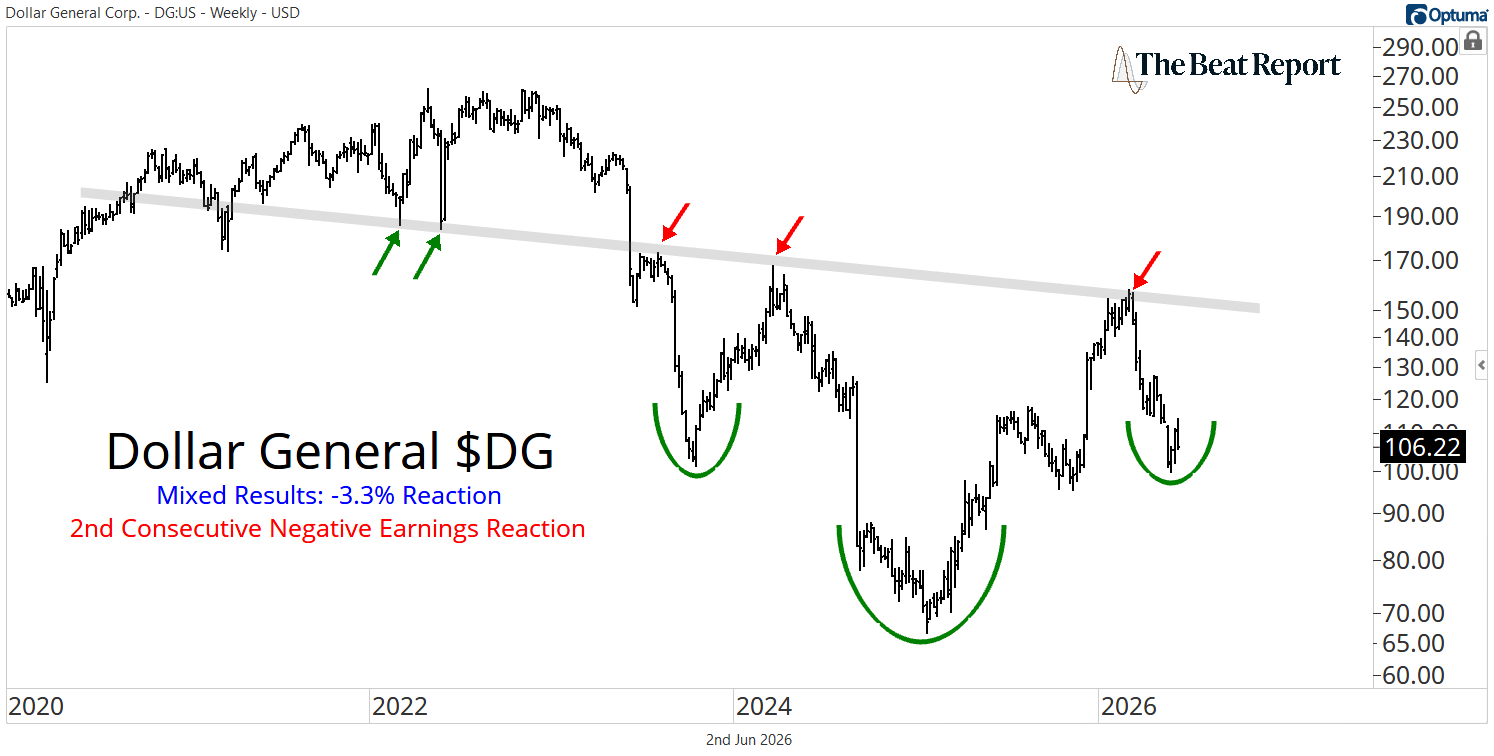

And in the same session, Dollar General $DG reminded us that not every stock is participating in this market the same way.

The S&P 500 closed higher by 14 basis points and notched another record high, but underneath the surface, Tuesday’s Beat Sheet gave us two very different stories.

*Click the image to enlarge it

One stock is being completely rerated as investors realize it has direct exposure to AI infrastructure, networking, and enterprise modernization.

The other is still stuck in repair mode after one of the nastiest drawdowns in its history.

Hewlett-Packard Enterprise was the clear standout.

HPE has gone from sleepy to vertical in just a few months. Since bottoming in late February, HPE has rallied more than 200%, and the advance has barely paused along the way.

HPE has been marching higher week after week, and it's now working on its 13th consecutive positive weekly candle.

What's clear is that the market loves everything this company is doing.

In their latest report, HPE reported record revenue of $10.68 billion, up 40% YoY, while non-GAAP earnings per share increased 108% over the same period.

Free cash flow reached $915 million, up $1.8 billion from the prior year, and orders more than doubled YoY, resulting in a record backlog.

This astronomical growth is why HPE is no longer trading like a forgotten legacy tech stock.

And until this uptrend shows signs of weakening, we expect HPE to remain a market leader.

On the other hand, Dollar General is a very different story.

The company reported mixed results and fell 3.3% in reaction to the news, marking its second consecutive negative earnings reaction.

DG is not the same kind of technical disaster we saw in some of the weaker retail names over the past few weeks, but it's still a stock with plenty to prove.

Dollar General was destroyed from its 2022 peak to its 2025 low, falling more than 70% during that bear market.

After a drawdown that deep, the repair process takes time.

And that's what we're seeing play out right now.

Dollar General is trying to carve out a massive inverted head-and-shoulders reversal pattern.

The right shoulder is forming near the $100 area, which makes that level incredibly important.

So long as DG holds above $100, the path of least resistance is sideways to higher in the short- to intermediate-term.

But the real line in the sand is closer to $160. Until Dollar General can break back above that area, this is still a repair job, not a confirmed primary uptrend.

Looking at Dollar General's YoY growth metrics, net sales increased 3.4%, same-store sales grew 2.0%, operating profit rose 10.8%, and diluted EPS increased 12.4%.

In other words, Dollar General isn't falling apart; it just has some work to do.

If you want access to our highest conviction technical and fundamental trades, join our growing community at the Premium Beat Report.

Thank you for your loyal readership,

-The Beat Team

Editor's Note: Everyone will hear about Securitize this summer, but Louis Sykes is more interested in the names nobody's talking about yet.