This stock just gave investors their first standalone look at one of the largest transportation companies in North America.

June 29, 2026

There are spinoffs, and then there are spinoffs that immediately become important market tells.

FedEx Freight $FDXF falls into the second camp.

This is an $18 billion freight operator with one of the most important less-than-truckload networks in North America.

In plain English, FedEx Freight moves the kind of freight that doesn't fill an entire truck by itself.

Pallets. Parts. Equipment. Inventory. Industrial goods. Regional shipments. The company moves time-sensitive freight.

That might not sound exciting at first glance, but this business sits squarely in the physical economy.

When freight companies are doing well, it usually says something important about industrial activity, manufacturing, small-business demand, and the flow of goods across the country.

Last week, we heard from the former parent company, FedEx $FDX, which reported a double beat but saw a slightly negative reaction in absolute terms.

However, the reaction score remained positive, suggesting the market treated that report better than the headline move implied.

On Friday, we got the first earnings reaction from the newly independent FedEx Freight.

And for a brand-new public company, it held up pretty well.

*Click the image to enlarge it

FedEx Freight reported revenue of $2.40 billion versus estimates of $2.22 billion.

And because this was the company’s first standalone report, we don't yet have a clean earnings-per-share comparison to work with.

So for our purposes, we're treating this as a mixed report until the earnings data becomes more complete.

The stock fell 2.9% on Friday, but the S&P 500 was also under pressure, which is why FedEx Freight still posted a positive reaction score.

A negative price reaction with a positive reaction score tells us the stock didn't really get punished as badly as the headline move suggests.

That means this reaction may have looked a lot different in a better tape.

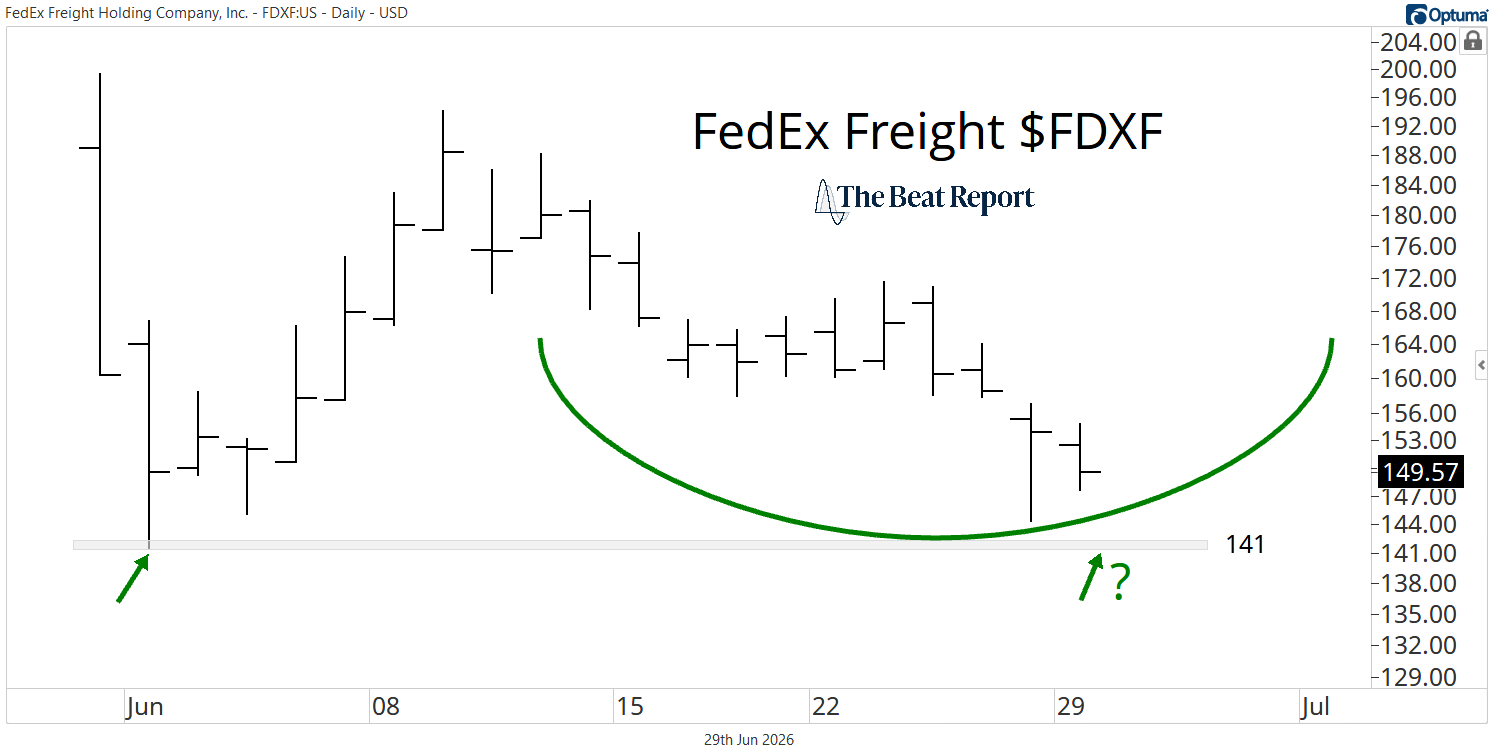

Now, here's a look at the chart of FDXF.

FedEx Freight began trading as a standalone company at the beginning of June, quickly found a low near $141, and then ripped higher during its first few days as a public stock.

Since then, it has spent most of the month giving back part of that initial move and carving out what looks like a potential accumulation pattern.

The key level is $141.

That marks the all-time low, and buyers recently showed up again near that same area.

So long as FDXF holds above that level, the stock is still building a constructive base during its first month as an independent company.

The fundamental story is also pretty compelling.

FedEx Freight generated $2.4 billion in revenue during the quarter, up nearly 5% YoY, while adjusted operating margin came in at 15.1%.

In other words, this is a profitable business right out of the gate.

Management also highlighted a few important early wins from the spinoff.

FedEx Freight now has its own dedicated LTL sales force, its own standalone website, a fit-for-LTL pricing system, and a cleaner operating focus as an independent company.

That may not make for the sexiest cocktail-party story in the world, but in freight, safety, reliability, pricing discipline, and service quality matter a lot.

This is a business where execution is the product.

One of the more interesting pieces of the story is the company’s dual-service model.

FedEx Freight runs one integrated network with two main service offerings: Priority and Economy.

Priority is the faster, time-sensitive service, while Economy gives customers a lower-cost option for more flexible freight.

Management says nearly half of its customers use both services, which gives FedEx Freight the ability to keep customers inside its own network instead of losing them to different competitors depending on whether they want speed or cost savings.

That's a real advantage if the company executes well.

So technically, FDXF is still too new to have a long-term trend, but the stock is carving out a constructive base above its early-June low.

Fundamentally, this is a profitable, scaled freight company with improving revenue quality and a clear standalone strategy.

And from an earnings sentiment perspective, Friday’s reaction was better than it looked on the surface because the stock posted a positive reaction score despite falling nearly 3%.

The stock needs more time, more data, and more earnings history before we can have the same level of conviction we have in more established trends.

But this is exactly the kind of new public company we want on our radar.

And that brings us to our next Beat Report Pitch Meeting.

These are the meetings we usually hold internally, where our Beat Team brings their highest-conviction trade ideas to Steve Strazza and debates them in real time.

For the first time, we pulled back the curtain and let members watch the process LIVE earlier this month.

And because of the overwhelming amount of positive feedback we've received, we're doing it again.

Our next Beat Report Pitch Meeting will take place on July 3, while the market is closed.

That gives us the perfect window to sit back, study the strongest setups, and pressure-test our favorite trade ideas without the noise of the trading day.

If you want access to the next pitch meeting, our current watchlist, and the next trade alert we send to members, join Beat Report today.

We hope to see you there!

Have a good Monday,

-The Beat Team

Editor's Note: Reading about ideas and acting on them are two different skills.

The SMTV Portfolio is where Spencer Israel takes the best of what crosses his desk from across the analyst network and trades it with real money.

He shows every entry and every exit to members in real time.