Pablo Picasso once said, “Every act of creation is first an act of destruction.”

That line captures where we are in markets better than any macro model or Fed speech.

For forty years, bonds were the smoothest trade in the world. Yields topped in 1981 and bottomed in 2020. You could close your eyes and buy Treasuries. Every panic, every shock pushed yields lower and bond prices higher.

Bonds weren’t just a trade — they were the foundation of modern portfolio theory. They offset equities, smoothed volatility, and gave investors a free lunch.

But creation requires destruction. That forty-year bull market has been destroyed. What comes next is the act of creation.

The End of Smooth

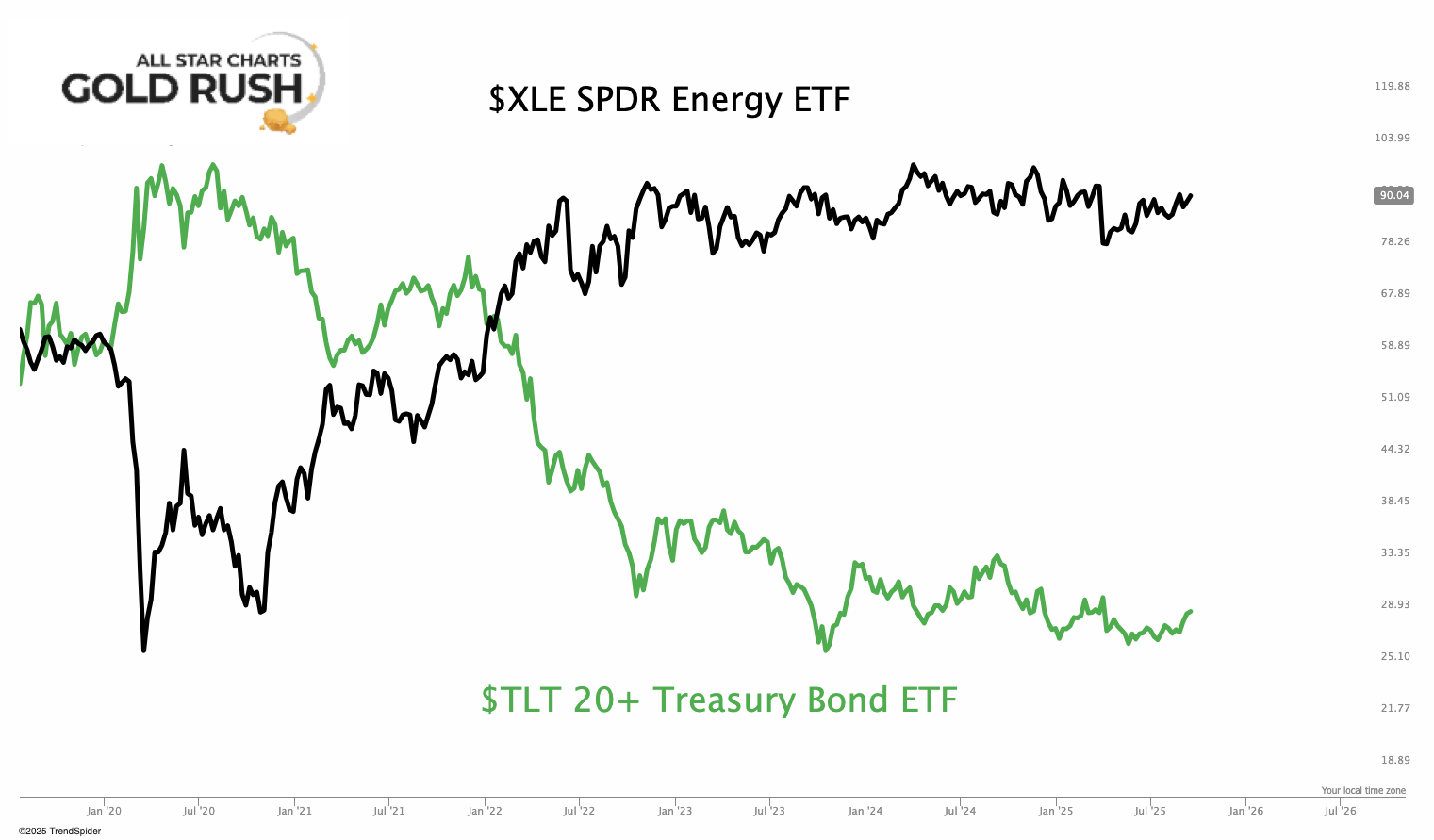

Look at the first chart.

In black: $XLE Energy ETF — the equity proxy for energy stocks.

In green: $TLT 20+ Year Treasury Bond ETF — the poster child of the 1980-2020 bond bull.

For years, investors could lean on TLT as their hedge. But since 2020, energy ripped higher while bonds collapsed. What was once the safest position turned into the market’s biggest widow maker.

That destruction matters. Because when the old safe haven dies, capital doesn’t sit still — it migrates. And the new home for capital is already visible: real assets.

Scarcity Breeds Creation

Commodity cycles are driven by fear and greed.

Fear at the bottom: Nobody wants them. Prices collapse, producers shut down, nobody digs.

Greed at the top: Everyone piles in. Supply explodes, OPEC pumps, frackers drill, miners expand. That oversupply kills the cycle.

At the bottom, destruction of investment creates scarcity. That scarcity lays the foundation for the next bull market.

Think back to 1999 — oil under $10, miners bankrupt, rare earths ignored. That destruction birthed the 2000s supercycle.

Think back to 1980 — peak inflation, everyone convinced commodities could only go higher. That greed birthed a twenty-year bear market.

Today looks like another one of those turning points.

The 40-Year Bond Cycle

The bond market runs on a forty-year rhythm:

1940s: Yields bottom.

1980s: Yields top.

2020: Yields bottom again.

Each pivot aligns with a shift in commodities.

1940s bottom → commodity bull of the 50s–70s.

1980s top → two decades of commodity destruction.

2020 bottom → the spark of a new cycle.

That’s not coincidence. Bond cycles set liquidity. Liquidity sets commodities.

Liquidity and the Dollar

Commodities don’t just move on supply and demand. They move on liquidity and the dollar.

Strong dollar cycles crush them.

Weak dollar cycles fuel them.

Expanding liquidity makes them roar.

Today:

Dollar rolling over.

Liquidity expanding again.

The bond hedge gone.

Capital has to flow somewhere, and it’s flowing into real assets.

Emerging Markets: The New Growth Engine

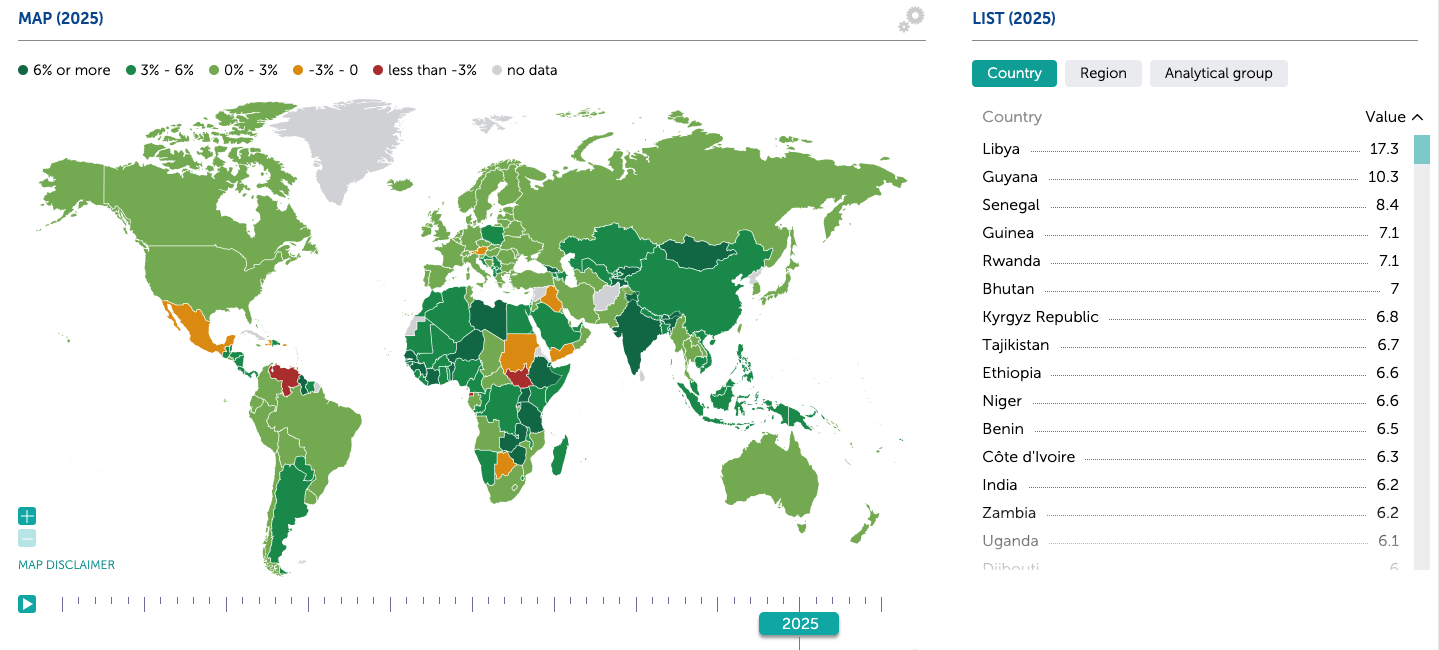

The second chart shows it clearly.

Growth rates across the world are strongest in emerging markets. Central America, Africa, Asia. Libya, Guyana, Senegal, Rwanda, India. These economies are compounding at 6%–17%.

Commodity demand doesn’t come from mature economies with flat demographics. It comes from the emerging world building infrastructure, electrifying grids, and expanding middle classes.

The growth of emerging markets is the demand side of the cycle. The destruction of the bond bull is the supply side. Together they create the new regime.

From Smooth to Volatile

The market is telling us something simple.

Bonds are no longer the hedge.

Mining stocks are the leaders.

Emerging markets are the growth engines.

The era of smooth, low-volatility returns is dead. That destruction has created something new: volatility, dispersion, commodity cycles.

Investors who cling to the past — who look to TLT as their anchor — will be fighting the last war.

Picasso’s line applies here too: you can’t create the future by holding onto what’s already been destroyed.

Fear and Greed in Motion

Fear is always where rebirth begins.

In 2020, nobody wanted oil — futures even went negative. Nobody wanted miners or agriculture. That destruction set the stage for today’s cycle.

Now, energy leads while bonds bleed. Commodities are waking up. Emerging markets are compounding faster than developed nations. Capital is shifting.

Greed will come later, just as it did in 1980 and 2008. But we’re not there yet. We’re in the early act — destruction giving way to creation.

The Signal in Yields

The question now is simple: what happens in the next few months?

Will the 30-year bond yield follow the Fed Rate?

If it doesn’t, that’s the signal.

It wouldn’t be surprising to see yields rise even as the Fed cuts rates. We’ve watched that happen before — rate cuts don’t always mean falling yields. Sometimes they light the fire.

Right now, the market is certain the Fed will cut. But the real tell isn’t the cut itself. It’s what happens afterward.

That reaction — whether yields roll over or keep climbing — will show us if this is just another reprieve… or the next leg of the cycle being born.