“Ending is better than mending.” — Aldous Huxley, Brave New World

Huxley wasn’t talking about the Federal Reserve, but he may as well have been. We’ve entered a market regime where policymakers would rather pump, patch, and prop than allow the system to correct.

And in that kind of world — a brave inflationary new world — the path of least resistance for markets is higher.

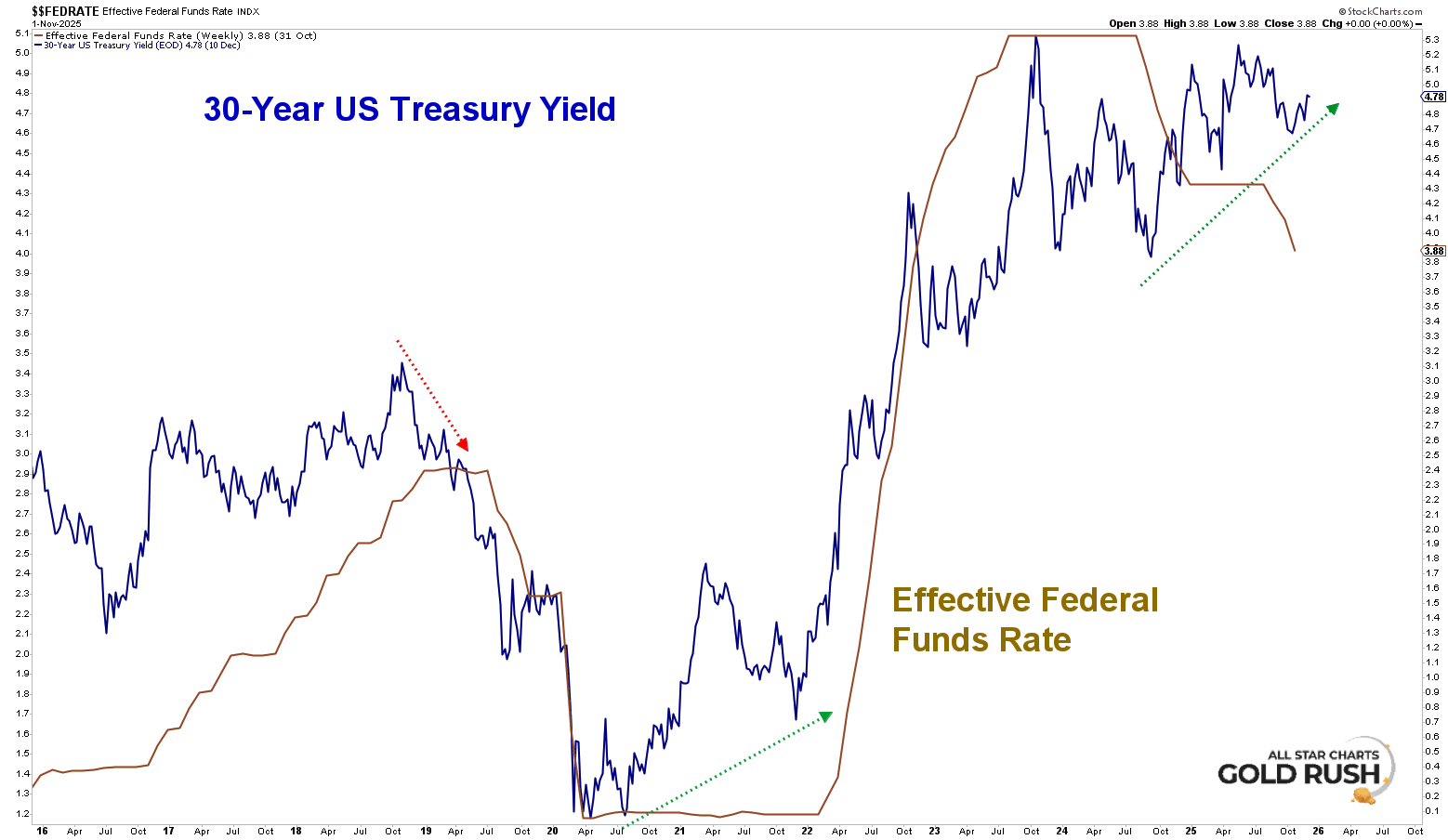

The Fed cut rates again this week, lowering the target range to 3.5%–3.75%, the third straight cut and the lowest level we’ve seen in more than three years. This wasn’t a unanimous move; the dissent was unusually loud. Several FOMC members openly pushed back, arguing inflation remains too elevated and labor markets too fragile to justify an easing cycle.

But dissent doesn’t stop the trajectory. Cuts are cuts. Liquidity is liquidity. And nothing stops this train.

The Long End Isn’t Buying the Story — It’s Pricing the Truth

“You can’t consume much if you sit still and read books.” — Brave New World

Nor can you slow inflation when fiscal and monetary policy both lean pro-growth. While the Fed is easing, the 30-year Treasury yield is rising. That’s not confusion — that’s clarity. When the front end drops and the long end climbs, the bond market is sending the strongest message it has:

Inflation is not finished. Nominal growth is re-accelerating. Money wants movement, not stillness.

This is the opposite of a recessionary curve. This is the opposite of “inflation defeated.” This is a forward looking market building expectations for higher prices, higher wages, higher economic churn, and higher equity valuations.

Huxley warned of societies engineered for comfort — where growth becomes compulsory.

We’re living a financial version of that world:

A system where policy is engineered to prevent contraction, regardless of the side effects.

Trump + The Fed: A Reflation Engine

Whether you love or hate the politics doesn’t matter. Markets don’t trade feelings — they trade flows.

With Donald Trump returning, the market is already pricing:

Fiscal expansion

Deregulation

Tariffs that raise domestic price levels

Reshoring incentives

A pro risk, pro growth spending regime

Pair that with a rate cutting Fed, and you get a liquidity profile that simply does not align with falling asset prices.

“Industrial civilization is only possible when no one thinks about it.” — Huxley

And here we are — an entire financial system drifting higher while most of the public insists on debating the wrong things. Inflation narratives come and go. Political noise comes and goes. But liquidity? Liquidity moves markets.

And liquidity is increasing.

Nothing Stops This Train

The Fed projects only one additional cut in 2026 — their attempt to look “responsible.” But their actions tell the true story: they’re easing into an inflationary environment, not away from one. Inflation expectations remain above target. Unemployment barely moves. And despite internal divisions, the policy path keeps drifting lower.

The long end keeps drifting higher.

And markets keep marching forward.

“History is bunk.” — Huxley

In our world, backward looking inflation data is bunk. Price knows first. Bonds confirm. Policy follows late.

We are not in a deflation cycle. We are not in a contractionary environment. We are not pricing recession.

We are in a Brave Inflationary New World — engineered by central banks, amplified by fiscal policy, and validated by the long end of the curve.