Seasonality and structure suggest a broader commodities breakout ahead.

By Sam Gatlin, Jason Perz

December 26, 2025

As we head toward the close of the year, commodities are quietly reaching an inflection point that’s easy to miss if you’re not looking at the big picture.

For most of this cycle, leadership has been narrow. Precious metals did the heavy lifting early, ripping higher and establishing clear primary uptrends.

More recently, base and industrial metals joined the move, confirming that the rotation was real and that it was broadening beneath the surface.

And we’ve spent a lot of time leaning into that strength, because that’s where the data has consistently pointed us.

Now, something larger may be underway.

The calendar is finally starting to cooperate.

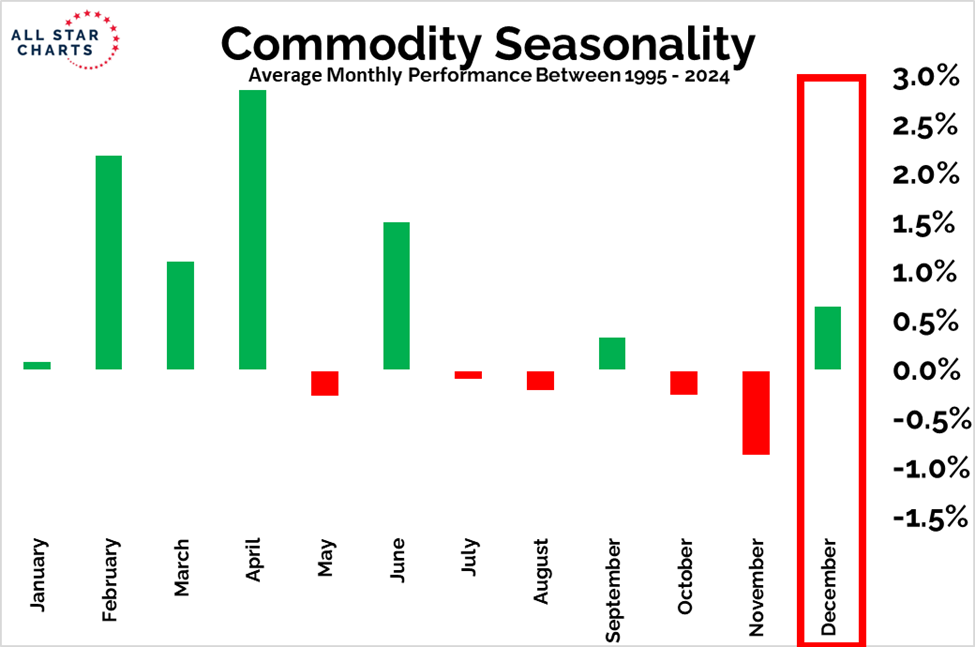

Historically, commodities perform best in the first half of the year and struggle during the back half.

November, in particular, has been a persistent drag on performance over the past several decades.

December, on the other hand, marks the turning point. From here, the seasonal tailwinds improve meaningfully as we head into the strongest stretch of the commodity calendar.

Seasonality, by itself, is never a reason to put risk on. But when the calendar begins to turn in sync with the technicals, it becomes an important piece of context.

And that’s precisely what we’re seeing now.

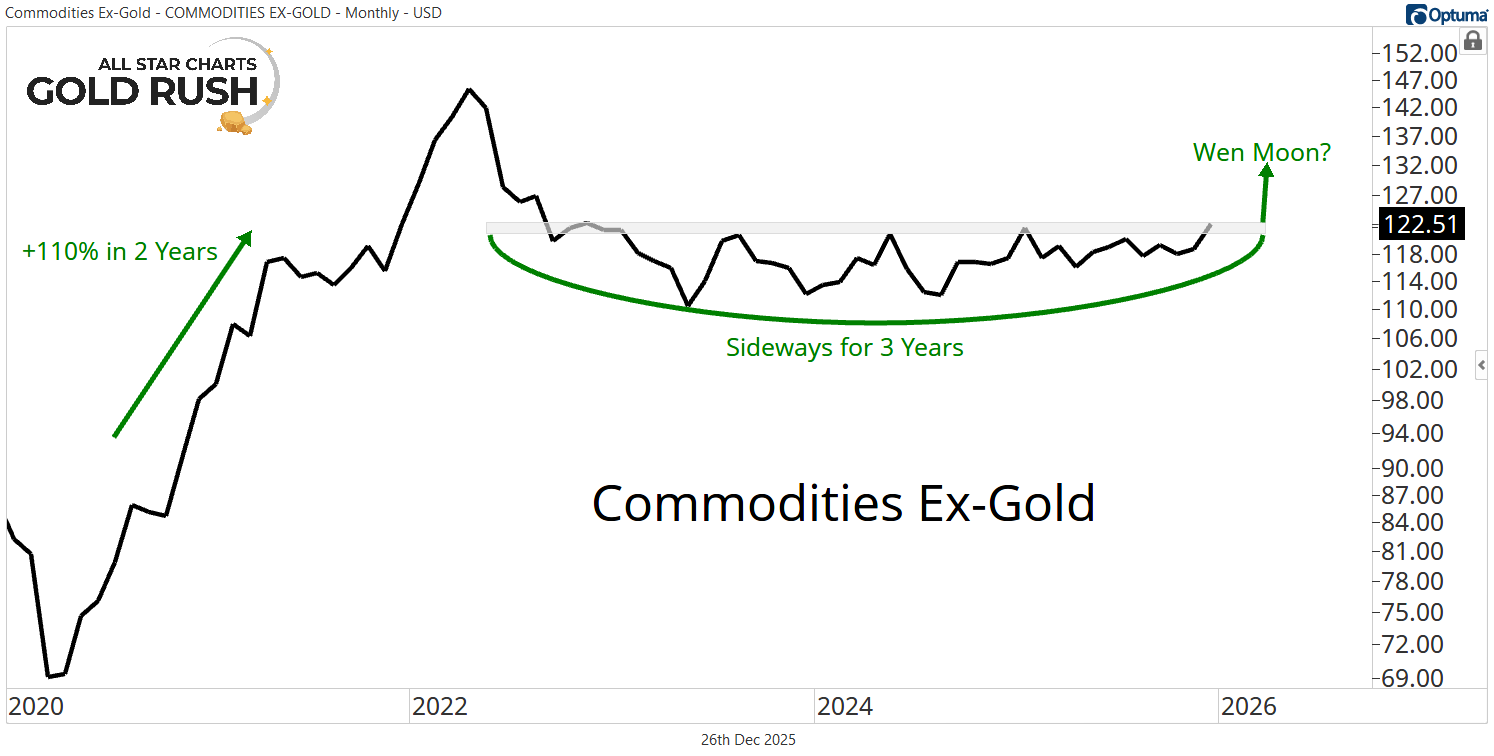

Our equal-weight basket of commodities ex-gold has spent the better part of the past three years digesting gains from the initial surge off the 2020 lows.

It has been a long, frustrating, sideways accumulation that allowed excesses to get worked off while stronger hands quietly built positions.

Now, that range is finally being tested.

Price is pressing against the upper boundary of that multi-year base, right as seasonal conditions are shifting from headwinds to tailwinds.

A decisive breakout from this area would signal a significant shift: from accumulation to expansion.

In other words, the point where commodities stop chopping investors to death and start trending again as a broader asset class.

We’ve already seen what the early stages of that expansion look like.

Precious metals have been relentless.

Base and industrial metals have followed, with Copper, Tin, Aluminum, and others confirming bullish primary trends.

At the same time, the laggards have stayed laggards.

Energy and agriculture remain mired in sideways-to-down trends, with many contracts still making new lows instead of new highs.

That divergence is not a bug; it’s a feature of how real cycles unfold. Expansion doesn’t happen all at once. It starts with leadership, then broadens outward over time.

A breakout in our commodities ex-gold index would be the signal that this broadening phase is underway.

It would tell us that the strength we’ve been seeing in metals is no longer isolated.

That capital is rotating beyond the early leaders.

And that the commodity bull market is entering its next act.

As always, our job isn’t to predict that outcome; it’s to recognize when the evidence is lining up.

Right now, we have improving seasonality, a prolonged accumulation pattern nearing its resolution, and clear leadership already in place.

That’s a powerful combination.

If this market is ready to expand, the charts will tell us, and we'll be here screaming from the rooftops about it.