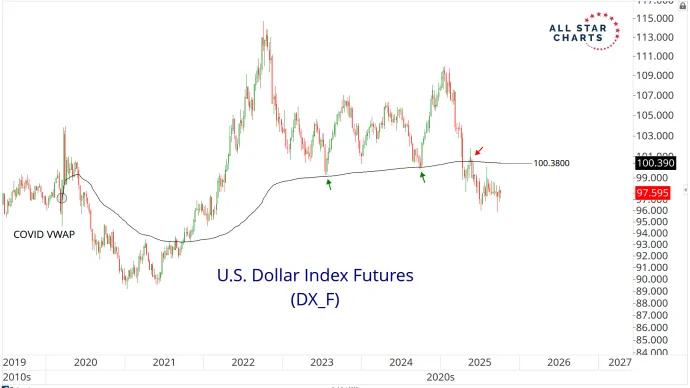

Risk assets are moving into risk-off territory, and it’s in environments like this where risk management separates tourists from traders, gamblers from speculators.

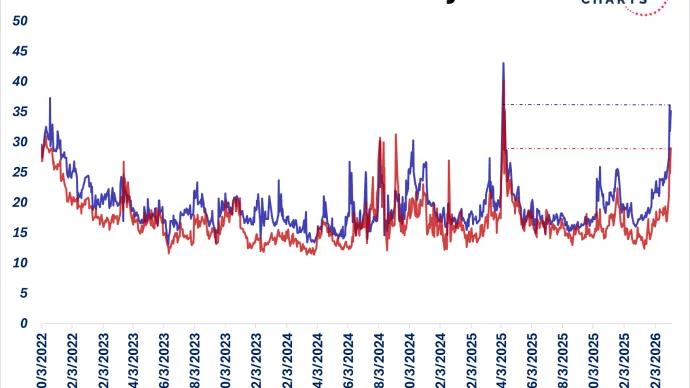

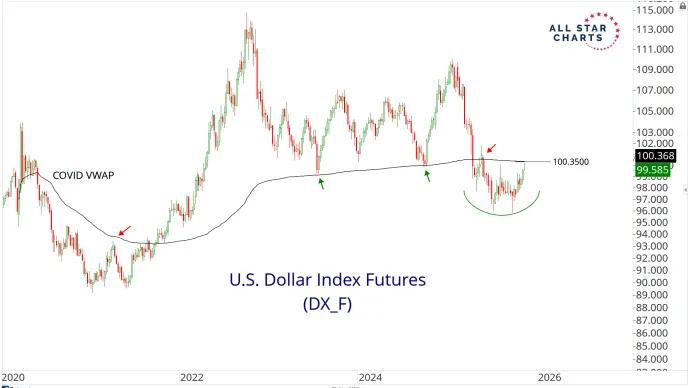

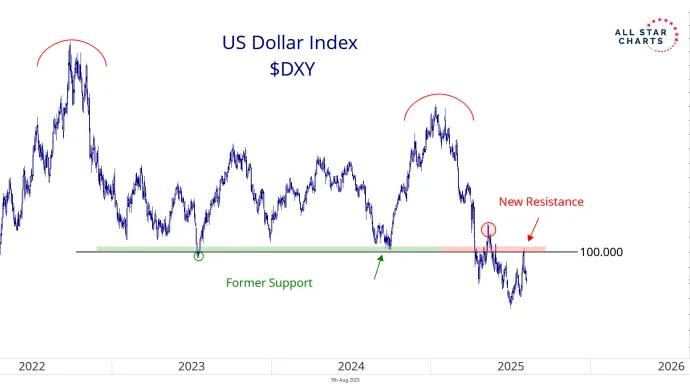

The US Dollar Index $DXY has been locked in a messy range for over a year, wobbling just enough to make everyone second-guess themselves, trapping bears on breakdown attempts and bulls on squeeze attempts.

When a structural trend reaches a turning point… expect volatility. We’re a month into 2026, and the US Dollar is already stirring the pot– making big moves and flirting with the completion of a major top.